Insurance for Finance & Mortgage Brokers

Policies meet MFAA and ASIC RG 210 requirements

Specialist cover for ARs and ACL holders

Professional Indemnity up to $10 million

Independent feedback based on verified reviews

Compare Quotes

From multiple insurers

Save Time

Buy online in minutes

Save Money

Switch and save

Instant Cover

Delivered to your inbox

Compare Quotes

From multiple insurers

Save Time

Buy online in minutes

Save Money

Switch and save

Instant Cover

Delivered to your inbox

Compare quotes from our trusted insurance partners:

On this page:

What does mortgage brokers’ insurance cover?

Mortgage brokers’ insurance is designed to protect your business, finances, and professional reputation. It can help cover the cost of common claims, such as:

- Professional or regulatory breaches

- Mistakes and errors in your work

- Lost documents

- Cyberattacks and data breaches

Mortgage brokers are required to have Professional Indemnity (PI) insurance under ASIC regulatory guide 210. It is also required to join the Mortgage & Finance Association of Australia (MFAA) and Finance Brokers Association of Australasia (FBAA). You must have a minimum of $2 million in PI insurance with at least 12 months run-off cover for membership.

BizCover has Professional Indemnity cover to meet regulatory and industry association requirements, as well as other tailored insurance options to help mortgage brokers protect themselves and their businesses.

Why do mortgage and finance brokers need insurance?

Practicing mortgage brokers are required to have Professional Indemnity insurance to meet regulatory requirements and obtain membership with industry associations, such as MFAA and FBAA.

Mortgage brokers routinely meet with clients, handle sensitive financial records, and provide specialised advice. These everyday business activities create risk for brokers, such as accidental property damage, paperwork delays, cyberattacks, and negligence claims. Insurance helps mortgage brokers cover the cost of these risks and more.

Meet ASIC regulatory requirements

Meet MFAA and FBAA membership requirements

Manage cyberattacks.

Pay legal costs if you face a liability claim

Enhance their credibility

Who needs finance & mortgage broker insurance?

Business insurance is essential for many types of finance businesses, including financial planning, investment consulting and many more, like

Mortgage broking services

Finance broking services

Home loan sales

Rural or community banking

Debt management

Unit trust management

Investment portfolio management

Financial advice or planning

Stock broking or trading

What types of insurance do finance and mortgage brokers need?

BizCover offers flexible policies designed to cover your business, services, and staff. Build an insurance package that suits your needs and buy in minutes

Basic insurance for mortgage brokers

Additional insurance for mortgage brokers

Let’s cover your small business on the go

Start a quote to see how much you can save and buy online in minutes.

How much does insurance for finance & mortgage businesses cost?

Business insurance for mortgage brokers costs $80 per month.

How is the cost of insurance calculated?

Risks of the industry

Cover level amount

Annual turnover

Number of Employees

Claims History

*BizCover’s Customer Average Monthly Payment Report is based on 1 July 20243 to 30 June 20254 and presented as a guide only. It may not reflect pricing for your particular business, as individual factors will apply.

Get flexible cover to match your needs

BizCover offers flexible cover limits to suit a range of mortgage brokers, from sole traders to growing businesses with high capacity.

Choose Professional Indemnity up to $10 million, Management Liability up to $5 million, and Cyber Liability up to $2 million.

Unsure how much to choose? Think about:

Statutory Profession Requirements

Cover required by contracts

Number of employees being covered

Your contract value

Worst case scenario claim size

Underinsurance

We know it’s tempting to select a lower level of cover to reduce premiums, but this can leave businesses shocked and insufficiently covered when making a claim.

Ways underinsurance catches business owners out:

Inflation

With inflation, the cost of living and doing business increases. Remember to over yourself, your tools and assets for the rising costs of replacing or covering them, not what you paid for them – you may be surprised at the difference.

Not covering the full cost of your risks

If you select cover levels for less than the value you may be found liable – left out of pocket when it comes to claims time. It’s important to review your risks and determine how much you will need to cover any claim that may come your way.

Factors influencing cost

Risk of the industry

Cover level amount

Annual turnover

Number of employees

Claims history

*BizCover’s Customer Average Monthly Payment Report is based on 1 July 20243 to 30 June 20254 and presented as a guide only. It may not reflect pricing for your particular business, as individual factors will apply.

Get flexible cover to match your needs

BizCover offers flexible cover limits to suit a range of mortgage brokers, from sole traders to growing businesses with high capacity.

Choose Professional Indemnity up to $10 million, Management Liability up to $5 million, and Cyber Liability up to $2 million.

This is the most you will be paid out if you need to make a claim.

Unsure how much to choose? Think about:

Statutory professional requirements

Cover required by contracts

Number of employees being covered

Your contract value

Worst case scenario claim size

Underinsurance

We know it’s tempting to select a lower level of cover to reduce premiums, but this can leave businesses shocked and insufficiently covered when making a claim.

Ways underinsurance catches business owners out:

Inflation

With inflation, the cost of living and doing business increases. Remember to over yourself, your tools and assets for the rising costs of replacing or covering them, not what you paid for them – you may be surprised at the difference.

Not covering the full cost of your risks

If you select cover levels for less than the value you may be found liable – left out of pocket when it comes to claims time. It’s important to review your risks and determine how much you will need to cover any claim that may come your way.

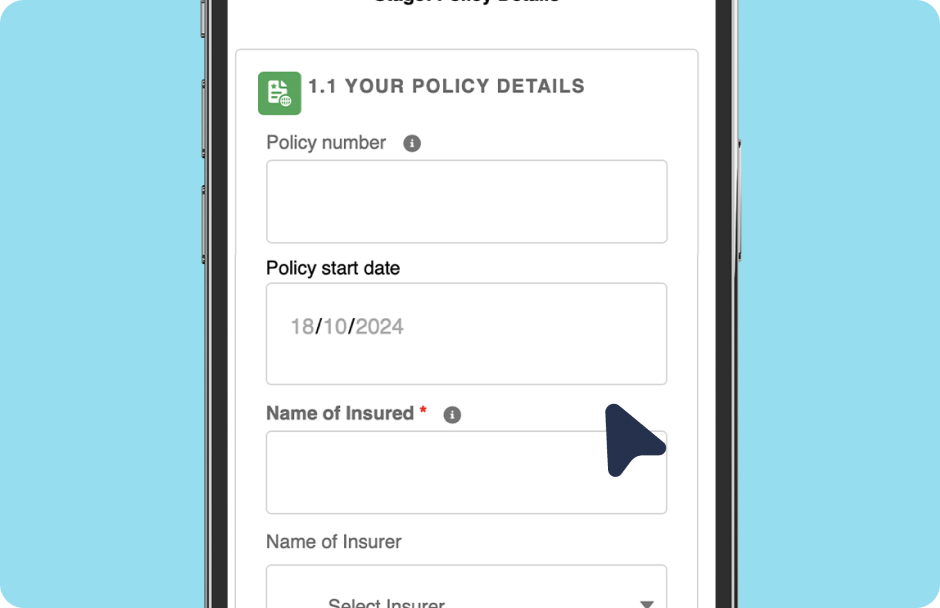

How It Works – Buying Online

5 easy steps to get instant cover online today

Select Profession

Pick Your Covers

Add Business Details

Compare Quotes

Get Covered Online

5 Steps to get your biz insured:

- Enter Occupation

Search & select your occupation

- Choose Cover(s)

Select the cover you need

- Business Details

Tell us about your business

- Compare Quotes

Compare prices & select quotes

- Get Cover Today

Instant policy docs to your inbox.

How To Make a Claim Online

We’ll assist you through the claims process & manage the claim directly with the insurer.

Let us know Fill out our

claims form and provide info

to support the claim

Receive extra support We

will assist you with your claim

Claim results We will notify

you of the claim outcome.

3 steps to get your biz insured:

- Let us know

Fill out our claims form and provide info to support the claim.

- Receive Extra Support

We’ll assist you with your claim.

- Claims Results

We’ll notify you of the claim outcome.

Award-Winning Tech & People

We’re not ones to blow our own trumpet, but we are pretty proud of our innovative insurance platform, outstanding team, and stellar workplace.

See How Much Other Finance & Mortgage Have Saved By Purchasing a Policy Through BizCover

Steve

Mortgage Broker from

NSW

Saved

$1,044

on

Professional Indemnity and Public Liability insurance

Patricia

Mortgage Broker from

VIC

Saved

$300

on

Professional Indemnity and Public Liability insurance

Mark

Mortgage Broker from

VIC

Saved

$300

on

Professional Indemnity insurance

^Savings made from February to August 2025. This information is provided as a guide only and may not reflect pricing for your particular business, as individual underwriting criteria will apply.

Frequently Asked Questions

Yes. Professional Indemnity insurance is required for mortgage brokers who hold a credit licence. Under ASIC regulatory guide 210, credit licensees who are not also regulated by APRA must have “adequate” Professional Indemnity insurance (unless alternative arrangements have been approved).

A Professional Indemnity policy is also required to join the Mortgage and Finance Associate of Australia (MFAA). To apply, you must provide proof of current insurance that:

– Has minimum cover of $2m per claim and $2m in the aggregate

– Provides at least 12 months of run-off cover

The amount of cover you may need depends on many factors, including the size of your business and the type of insurance you are considering. For example, mortgage brokers must have “adequate” Professional Indemnity insurance to hold a credit licence under ASIC regulatory guide 210. This means that a sole trader may need a different level of PI cover than a larger brokerage. The amount of PI cover you need may also be determined by client contracts. Other types of insurance may depend on the size of your business and how you operate.

Yes. Mortgage brokers are required to have Professional Indemnity insurance under ASIC regulatory guide 210, regardless of where their business is located.

Other types of insurance, such as Public Liability or Contents cover, may also be necessary for home-based mortgage businesses. Household building & contents policies typically do not cover business activities. You may need separate business policies to cover things such as client injuries or property damage, lost records, or damaged equipment (like a laptop or printer).

A retroactive date is the earliest date from which your insurer will cover a claim. Claims made after the retroactive date will generally be covered, whereas claims made before that date will be denied.

With BizCover, your certificate of currency is emailed to you immediately after purchasing a policy. You can also download additional copies at any time by logging in to our customer portal.

Hear from our customers

Easy to organise the cover

Bushra

Great service and guidance given by the operator

Manpreet

Very easy platform to navigate, Competitive quotes

Dave

Prompt polite service from helpful knowledgeable person. thank you Stephanie

Anne

Quick response from your team & great customer service loved it

Satheesh

Real-life customer reviews verified by Feefo